What Is IUL Insurance? A Plain-English Guide to Indexed Universal Life

Indexed Universal Life insurance explained in plain English: how it works, the floor and cap, the real advantages and tradeoffs, and who it's actually for.

Published May 28, 2026 · 10 min read

Indexed Universal Life (IUL) insurance is a type of permanent life insurance that provides a death benefit while also building cash value based on the performance of a stock market index, such as the S&P 500. Unlike investing directly in the market, IUL policies typically include a floor that protects against losses and a cap that limits gains.

In plain English: IUL combines lifelong life insurance protection with the potential for tax-advantaged cash value growth.

What Is IUL Insurance?

Indexed Universal Life Insurance — commonly called an IUL — is a form of permanent life insurance designed to provide lifelong coverage while allowing the policyholder to accumulate cash value over time. The cash value portion is linked to the performance of a stock market index such as:

- S&P 500

- Nasdaq 100

- Russell 2000

- Dow Jones Industrial Average

Your money is not directly invested in the market. Instead, the insurance company credits interest to your policy based on the index's performance, following the specific rules outlined in your contract.

How Does IUL Insurance Work?

An IUL policy works through four basic steps:

- You pay premiums into the policy.

- A portion is deducted to cover the cost of insurance and policy expenses.

- The remaining funds enter your cash value account.

- Cash value earns indexed interest based on the performance of a selected index.

The Three Main Parts of an IUL Policy

| Component | Purpose |

|---|---|

| Death Benefit | Provides money to beneficiaries when the insured passes away |

| Cash Value | Builds tax-advantaged savings over time |

| Index Strategy | Determines how interest is credited |

Each room serves a different purpose: the protection room (death benefit), the growth room (cash value), and the access room (policy loans and withdrawals).

How IUL Cash Value Growth Works

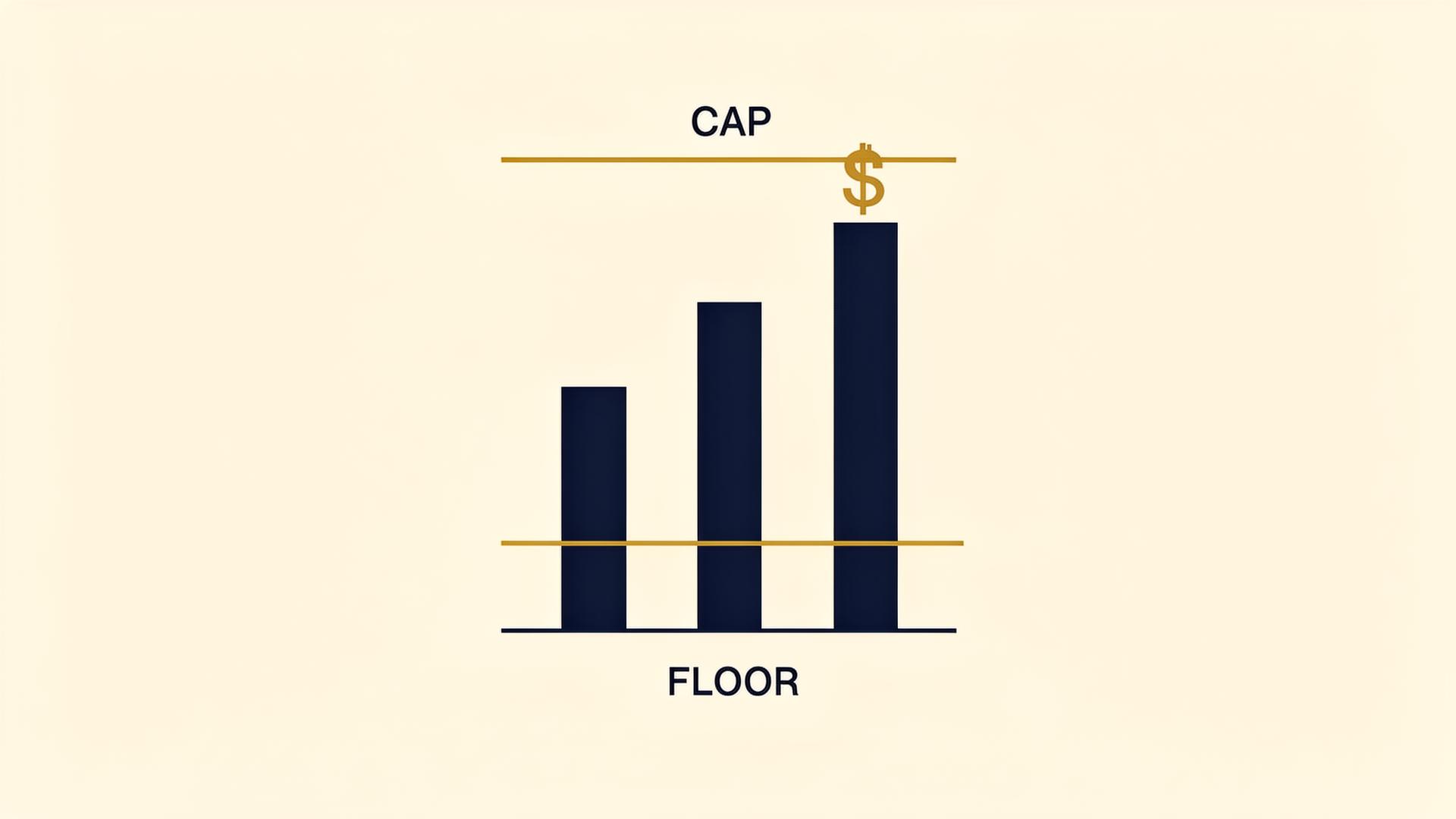

Two concepts make IUL unique: the floor and the cap.

The Floor

Most IUL policies include a 0% floor. If the market declines, your credited interest does not go below the floor.

The Cap

Most policies also include a cap rate. If the index gains more than the cap, your credited interest is limited.

| Year | S&P 500 Return | IUL Credited Rate |

|---|---|---|

| 1 | +18% | 10% (cap applied) |

| 2 | -12% | 0% (floor applied) |

| 3 | +8% | 8% |

| 4 | +15% | 10% (cap applied) |

“The goal of an IUL is not to outperform the stock market. The goal is to reduce downside risk while participating in a portion of market gains.”

7 Advantages of IUL Insurance

- Permanent coverage that can last your entire lifetime.

- Tax-advantaged growth — cash value grows tax-deferred.

- Potential tax-free loans against accumulated cash value.

- Downside protection through the policy floor.

- Flexible premiums that can often be adjusted.

- Estate planning benefits — death benefits generally pass income-tax free.

- Retirement income potential as part of a broader strategy.

7 Disadvantages of IUL Insurance

- More complex than term life insurance.

- Fees and expenses can be significant, especially in early years.

- Caps limit upside potential in strong market years.

- Requires a long-term commitment to perform as designed.

- Poorly designed policies can underperform.

- Not ideal for everyone — suitability matters.

- Illustrations are projections, not guarantees.

Who Should Consider an IUL?

An IUL may be appropriate for:

- High-income earners

- Business owners

- Individuals seeking permanent life insurance

- People concerned about future taxes

- Families focused on legacy planning

Who Should Avoid an IUL?

An IUL may not be suitable for:

- People needing the cheapest life insurance option

- Individuals with limited budgets

- Investors seeking maximum stock market exposure

- Those who only need coverage for a short period

IUL vs Other Types of Life Insurance

| Feature | IUL | Whole Life | Term Life |

|---|---|---|---|

| Lifetime Coverage | Yes | Yes | No |

| Cash Value | Yes | Yes | No |

| Market-Linked Growth | Yes | No | No |

| Lowest Cost | No | No | Yes |

| Flexible Premiums | Yes | No | No |

Frequently Asked Questions

- What does IUL stand for?

- IUL stands for Indexed Universal Life Insurance.

- Can you lose money in an IUL?

- Most policies include a floor that protects against negative index returns, although policy expenses still apply.

- Is IUL better than a 401(k)?

- Not necessarily. They serve different purposes and are often used together.

- Is IUL a good retirement strategy?

- For the right person, an IUL can be one component of a broader retirement plan.

- How long does it take for an IUL to build cash value?

- Most policies are designed as long-term strategies and may take several years before meaningful cash value accumulation occurs.

Final Thoughts

Indexed Universal Life Insurance can be a powerful financial tool when designed properly and used for the right purpose. It is not a magic investment, and it is not appropriate for everyone.

The best way to determine whether an IUL fits your goals is to understand how it works, compare your options, and review a personalized illustration based on your age, goals, and funding strategy.

Keep reading

All posts

What Does IUL Stand For? (IUL Meaning Explained Simply)

What does IUL stand for? Learn the meaning of Indexed Universal Life Insurance, how it works, key features, pros and cons, and common misconceptions.

May 29, 2026 · 7 min read

Caps, Floors, and Participation Rates Explained

The three numbers that determine what your IUL actually credits — and which one carriers change without telling you.

April 2, 2026 · 7 min read

What 'Maximum-Funded' Actually Means

Two policies with identical premiums can have radically different outcomes. The difference is design.

February 4, 2026 · 7 min read